HK Economy

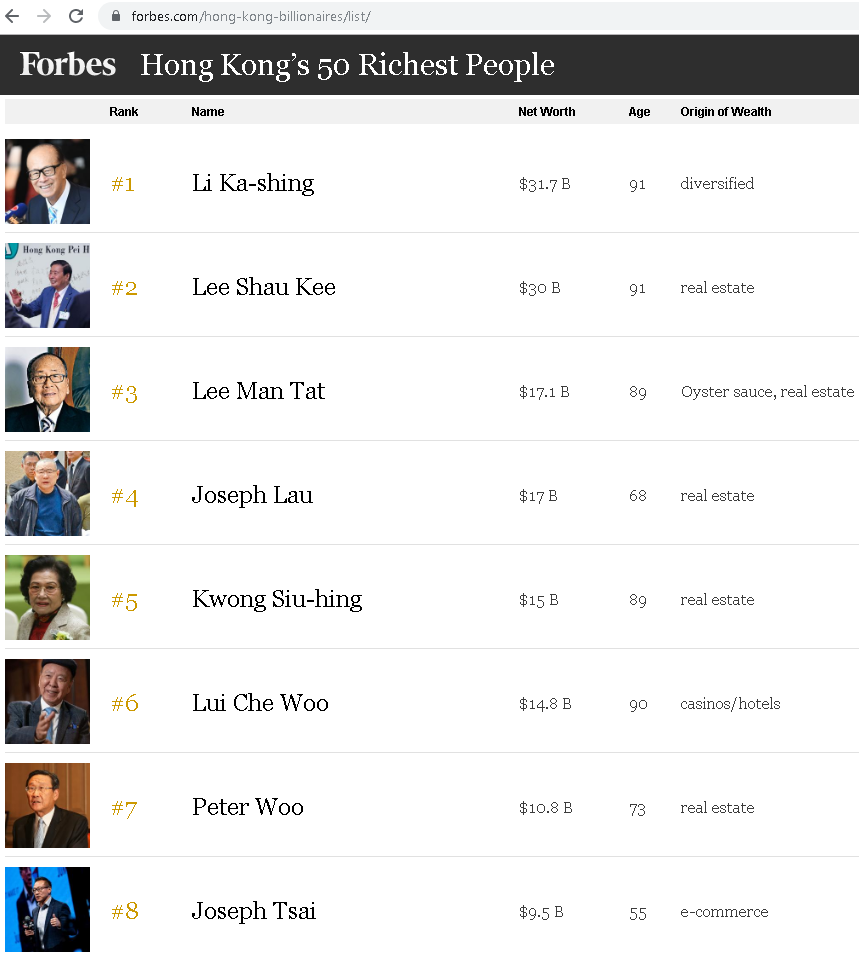

Normally, when you see a few cockroaches coming out of the kitchen, you know that there are a lot more to come, and we should expect volatile movements for an average of 1.5 years. At this point, my gut feel is that the protests are manifestations of deep underlying issues in how the society has divided the rich and poor. They don't have a wealth equalisation mechanism to uplife the poor, and the property-rich moguls control a lot of real estate and the government only provides rental housing for the really poorest of poor. Many younger workers "sandwiched" in-between are forced to buy either expensive property built by companies owned by these billionaires or rent from the many millionaires. If there are going to be any reforms, it will just be the beginning of a new era, and any equalisation will probably take a generation to take effect. In the meantime, the rich will just continue to get richer and for any aspiring investor, these billionaires are real examples of the effects of compounding. You can peek into forbes list of HK billionaires.

I am generally confident that property prices won't drastically fall suddenly because it takes a lot of stars to align for that to happen, but systemic issues can cause property prices to fall over 20 years, and this is the scary part, because you may not notice it, and by the time you notice it, you will realise that you didn't earn anything. The key metric I look at is population growth. Population growth is the main driver for economic growth. However, at a certain point, if the growth outpaces the infrastructure growth in the country, the country will be unable to support and will need to pause the growth, catch up in infrastructure (land expansion, utilities, transport, housing) investment, deal with a bit of oversupply issues, then let population grow again. You can see this being played out when you plot the growth rate over time.

In this chart, HK and Singapore's growth rate goes in cycles. Since 1997, HK's growth has been between 0-1%. I interpret it as infrastructure has been under stress to support the population for 20 years. How do we know if the government is doing its job in infrastructure investments to support population growth? I look at the population density metric.

In this chart, the year where the two lines crossed is 2007. When I see this, all things equal, I don't know what the future will be, but I can infer that the Singapore government is doing a lot more to support the population growth, i.e. chiefly land expansion. This also means that Singapore has a higher chance of over supply issue than HK. If you already hold properties in Singapore and HK, it's likely that the capital appreciation in HK is faster because the supply is increasing at a slower pace in HK. I won't want to invest in a Singapore residential property at the very least.

How all these can play out in an extreme scenario is where the poor in HK move to cheaper cities in China, much like how the poor leave the expensive cities in the bigger countries such as US and Canada. However, whether they get to live in more human conditions (as opposed to toilet-sized homes) is something I don't know because theoretically, they could have left HK to leave in a cheaper place, but they probably feel that HK is their home and refuse to move. Hypothetically, if HK had been a China all the while, the people would have behaved more like a US citizen shifting from expensive Manhattan to cheaper Texas, and still feel at home. In any case, expensive cities typically become more and more expensive over time. HK is a city, and not a country, so it's really not easy for their economy to crumble. On the flipside, an oversupply issue can be a massive drag on Singapore's economy.

Hongkong Land (HKL)

So I am confident of the HK economy, and I will get into the financials of HKL. HKL has 2 sources of income, rental (investment) and development sales. Development sales is something hard to value because income recognition will be lumpy, so I will not go too deep into it. I will just value the rental income aspect, and treat the development sales income as a bonus.

First, I want to know what's the proportion of "recurring investment income", so I will add the rental income and income from associates. This is the stable part of income that I know can be retained by the company or paid out as dividends.

In 1H2019 financial report (page 11 of 21), rental and service income was US$509.6M + US$75.3M = US$584.9M. Operating profit for investments (rental) was US$482.6M. I deduce rental expenses to be 17.5% (1-482.6/584.9). In 1H2018, the equivilent was 19% (1-456.6/(484.1+76.4)). Associates contribute US$127.2M.

Recurring investment income for 6 mth = operating profit for investments + associates income - finance expense - operating costs

= 482.6M + 127.2M - 59.4M - 334M

= US$216.4M

as a % of profit before tax (page 5 of 21) = 216.4M/537.7M = 40%

In reality, the expenses will be lower because I took the whole figure, which include the costs for the development sales. There was no breakdown available in the financial report. This is a conservative calculation, but it means 40% of income is recurring in nature. Its income is also fairly stable as the vacancy rates are between 1-3%.

Next, I want to know if this income can sustain the dividends paid out.

Dividend paid out in 2018 = 16 cents/share = US$373.4M (page 14 of 21)

Recurring investment income for 12 mth - 17% corporate tax = 216.4M x 2 - 17% = US$359M.

17% is a conservative rate too. This should be lower as they will have deductibles. Debt to Equity is 9-10% which means dividends are not paid out of debt. I am inclined to believe that the dividends are sustainable.

Next, I want to know the Return on Asset, which is how much juice the company can squeeze out of its assets, which is like the yield on assets, or rental yield. Unfortunately, HKL doesn't publish its cost price, so we can't calculate a yield on cost.

Investment asset value = US$33,815.4M (page 7 of 21)

Associates asset value = US$7,152.5M

Total = US$40,967.9M

Net Return on Asset = 216.4M x 2 / 40,967.9M = 1%

Gross Return on Asset = (482.6M + 127.2M) x 2 / 40,967.9M = 3%

Gross Return on Asset (property only) = (482.6M) x 2 / 33,815.4M = 2.85%

The net Return on Asset is actually quite low, but this is not the real yield on cost, which should be lower especially if the properties were bought long ago. This is the yield based on current market value, so I interpret this as the properties market value are overvalued, because 1% is lower than safe bond rates of 1.5%-2%. If we assume property valuation to fall to a safe bond rate of 2%, this means we can expect the investment values to reduce by 50%. If we expect safe bond rates of 3%, we can expect the investment values to reduce by 33%.

Finally, I want to know the Price to Book value, but I want to be more conservative and calculate an adjusted book value, and not use the book value calculated by the company which uses current market values of their investment properties. I won't want to just apply a discount rate to the NAV because in the event of a market crash, the assets will half in value, but the loans will remain at 100% and won't be halved.

Net asset value (NAV) per share = US$16.50 (page 1 of 21)

NAV = US$38,529M (page 7 of 21)

Number of shares = 2,333.9M (page 13 of 21)

My adjusted NAV = US$38,529M - 50% of (investment properties, joint ventures, properties for sale) - debtors = US $38,529M - 50% x ($40,967.9M + $2,065.8M) - $985M = US$16,027.15M

My adjusted NAV per share = US$6.87

Price to my adjusted NAV = 5.40/6.87 = 79% (i.e. 21% discount)

Price to unadjusted NAV = 5.40/16.50 = 33% (i.e. 67% discount)

[30 Oct Edit: Discounted joint ventures, properties for sale, debtors into the adjusted NAV to reduce the NAV further]

Valuation

If I assume a value buy to be at the cost of 60% of the asset values, the max price to buy is 60% of US$6.87 = US$4.12.

At last done price US$5.40, US$0.16 dividend = 0.16/5.40 = 3% yield

HKL will be an asset play as there is a discount. The % varies, depending on how you value their assets. The dividends are so-so, however if market depresses the market price further to US$4.12, all things equal, it turns into a dividend play at 4% yield, with a margin safety of -50% discount to market value for its investment assets.

The last done price was US$5.40, which is attractive enough for me, so I should be nibbling some in the coming week.

The writer does not hold shares in HKL.