I picked this e-book from the online library (National Library Board - Overdrive) as it was available and I didn't have to deal with a hardcopy book reservation and pick up. It was really convenient to read the e-book.

The book is about an ex-trader who believes that traders deal with random events everyday. The whole book is about his musing about different aspects of randomness that he has noticed in traders and why he didn't agree with them. For example, he believes that the guys who follow trend analysis to buy and sell stocks are simply lucky that they are buying and selling in an uptrend, so anybody would have made money. And these guys will be so convinced that they have the skills to analyse trends that they convince themselves that once in a while, when there are unexpected/unpredictable events, they will be "wrong", and find some excuse to convince themselves that they are still right.

It made me reflect about the way rewards are structured in a fund house. Outcomes are favoured and many times, outcomes can't really be controlled too. One fund manager may be luckier and gets a 20% return, whereas another fund manager may be less lucky and gets a 2% return. On paper, the one with the 20% is better. There may be also other funds with -20% return, that will never be on the recommendation list to customers until it yields a positive return. When customers look for fund managers, they only look for those with high returns, and they ignore everything else because returns are all that counts. While there may be some truth behind position sizing, asset allocation, diversification strategy, risk assessments, if we think about it logically, it boils down to fundamental analysis, i.e. whether or not there is an income-generating element. It amazes me how some people can convince themselves to part with their money and trust fund managers that do not even disclose the underlying assets. What if they are just buying a bunch of lottery tickets?

If you would like an alternative take to looking at stock markets, this is a really good book because it introduces the concept of probability, and after reading it, I am quite sure that you even doubt fundamental analysis. The authors suggests that you have nothing certain, which is true, you don't know what will happen tomorrow, and although probability of these unpredictable events are low, the impact can be very high to wipe out everything. Thinking about how some companies become bankrupt is a good example, despite what people say about the fault lying in poor financial management and all, there are many companies with poor or worse financial management too, yet they survive, so there is really no way to tell when these companies will go bankrupt.

Survivorship bias is another topic that really resonated with me because it am always told to follow "tried and tested methods", follow that the boss says, etc. What worked in the past may not always work in the future. While there is a low probability of the "may not work in the future" event happening, the impact, if of the event can be very severe, for example, you may not have enough time to change a system, may not have enough time to raise money to do certain things you need to do, etc. Always thinking and assessing every situation, no matter how routine, is essential.

Buying with probability of events in mind will certainly help factor in margin of safety, which is the principle preached by Graham. As a whole, the author advocates being conscious about randomness, so that we don't become overly complacent, we don't think get controlled by emotions, we are mindful when luck plays a part, we don't show-off, we make decisions with more awareness of possible outcomes to set realistic expectations so that we don't get crushed by black swan events. I am certainly heading to his next book The Black Swan next.

Monday, November 26, 2018

Friday, November 16, 2018

How much have I earned and lost in 2018?

How much have I earned and lost in 2017?

I am writing this earlier this year as the total amount should be more or less the same by year end. Objective for 2018: Increase REITs by 10%, increase portfolio yield by 0.5%, increase income to $14,000.

Verdict: Didn't meet, didn't meet, meet.

Average dividend yield in 2017 was 4.56%. I didn't meet my target, and my average yield was 4.73% this year. This was achieved by buying stocks with >5% yield to increase the average, but it got pulled down by other non-performing stocks that cut dividends. In 2017, the plan was to support the increase by increasing REITs to 50% of my portfolio, starting from REIT ratio of 23% in 2017, and slowly rebalancing and capital injection at the right prices over 3 years, from 23% -> 33% -> 43% -> 50%. I did not buy that many REITs. In fact, I bought Singtel instead because yields were more attractive than REIT yields.

In order to further increase the average yield by another 0.5% will not be as easy as it will require buying stocks with >6% yield to increase the average. I may want to increase the growth stocks proportion, but I will see how prices are next year.

Income was $15,500 ($1,290/month), so I exceeded the target of $14,000. The additional increase was due to better dividends and also high bank interest rates from Bank of China 2.75%, UOB One 2.43%, Hong Leong Finance 1.7%, CIMB Fastsaver 1%, Singapore Savings Bonds 1.8%.

I didn't increase my Autowealth portfolio much as I found the prices too eratic. I will continue to contribute $400/month after the prices reverse closer to the mean. After an insane annualised yield of 15% in 2017, in 2018, the returns are a mere 4%, and could have been lower if I had continued to contribute as prices escalated 2% per month only to watch a big fall a few months later.

Unrealised profits/losses:

Autowealth = S$50 (+$260 in 2017)

Singapore Stocks = -$20,000 (+$20,000 in 2017)

Overall, gains in 2017 had been reversed to losses.

Objective for 2019: Increase REITs by 10% (Trying this again, hope to have good bargains), increase portfolio yield by 0.5%, increase income to $16,800 (or $1,400/month).

Lifetime accumulated dividends and interest, net of losses, excluding portfolio valuation gain/loss = $65,000

I am also sticking to my slow and steady turtle income "methodology": Assuming that I continuously invest $36,000/year or $3,000/month,

In 2 years, accumulated dividends and interest = $100,000, $1,600/month

In 6 years, accumulated dividends and interest = $200,000, $2,200/month

In 9 years, accumulated dividends and interest = $300,000, $2,700/month

It may seem slow, sticking to $3,000/month for 10 years without factoring any increases, but I prefer the approach of buying on dips, which may not be the most optimal thing to do, but I feel that it helps to make my stock acquisitions dividend accretive (portfolio cost price wise). If there is a big market correction or flash crash then I will likely activate my warchest.

I am writing this earlier this year as the total amount should be more or less the same by year end. Objective for 2018: Increase REITs by 10%, increase portfolio yield by 0.5%, increase income to $14,000.

Verdict: Didn't meet, didn't meet, meet.

Average dividend yield in 2017 was 4.56%. I didn't meet my target, and my average yield was 4.73% this year. This was achieved by buying stocks with >5% yield to increase the average, but it got pulled down by other non-performing stocks that cut dividends. In 2017, the plan was to support the increase by increasing REITs to 50% of my portfolio, starting from REIT ratio of 23% in 2017, and slowly rebalancing and capital injection at the right prices over 3 years, from 23% -> 33% -> 43% -> 50%. I did not buy that many REITs. In fact, I bought Singtel instead because yields were more attractive than REIT yields.

In order to further increase the average yield by another 0.5% will not be as easy as it will require buying stocks with >6% yield to increase the average. I may want to increase the growth stocks proportion, but I will see how prices are next year.

Income was $15,500 ($1,290/month), so I exceeded the target of $14,000. The additional increase was due to better dividends and also high bank interest rates from Bank of China 2.75%, UOB One 2.43%, Hong Leong Finance 1.7%, CIMB Fastsaver 1%, Singapore Savings Bonds 1.8%.

I didn't increase my Autowealth portfolio much as I found the prices too eratic. I will continue to contribute $400/month after the prices reverse closer to the mean. After an insane annualised yield of 15% in 2017, in 2018, the returns are a mere 4%, and could have been lower if I had continued to contribute as prices escalated 2% per month only to watch a big fall a few months later.

Unrealised profits/losses:

Autowealth = S$50 (+$260 in 2017)

Singapore Stocks = -$20,000 (+$20,000 in 2017)

Overall, gains in 2017 had been reversed to losses.

Objective for 2019: Increase REITs by 10% (Trying this again, hope to have good bargains), increase portfolio yield by 0.5%, increase income to $16,800 (or $1,400/month).

|

| Chart of humble beginnings |

I am also sticking to my slow and steady turtle income "methodology": Assuming that I continuously invest $36,000/year or $3,000/month,

In 2 years, accumulated dividends and interest = $100,000, $1,600/month

In 6 years, accumulated dividends and interest = $200,000, $2,200/month

In 9 years, accumulated dividends and interest = $300,000, $2,700/month

It may seem slow, sticking to $3,000/month for 10 years without factoring any increases, but I prefer the approach of buying on dips, which may not be the most optimal thing to do, but I feel that it helps to make my stock acquisitions dividend accretive (portfolio cost price wise). If there is a big market correction or flash crash then I will likely activate my warchest.

Monday, October 29, 2018

Stock Review: ISOteam

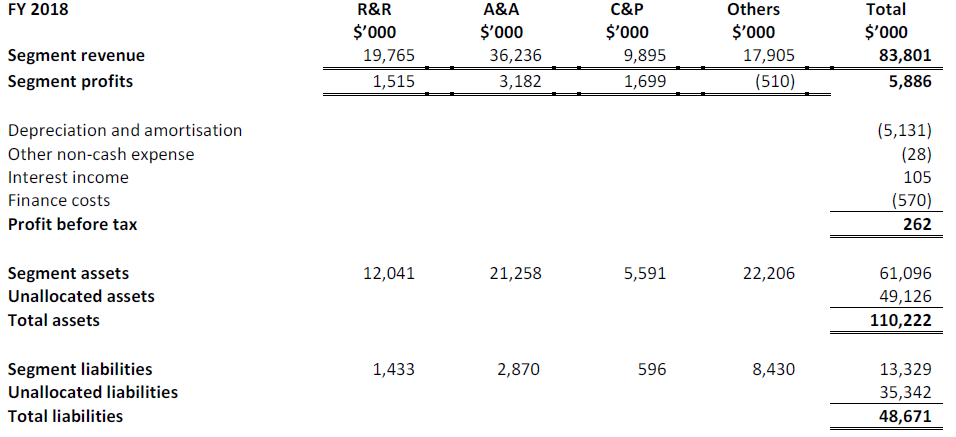

ISOteam Limited is a company that started out as painter that diversified its business over the years. It is Nippon Paint’s exclusive applicator of paint works for Repairs and Redecoration (R&R) projects for the HDB and Town Council segments, likely through its joint venture subsidiary TMS Alliances Pte Ltd.

The share price for this company had recently fallen a lot, because of fewer projects, reduction in suppliers' rebates (hence increased cost of sales) and increase in marketing expenses that ate into profits.

Business Model

65% of revenue comes from R&R and Additions and Alterations (A&A), which are rather labour-intensive. It's one of those things like a hair cut where you need hair cuts regularly and it can't exactly be automated. For hair cuts, the demand scales proportionally to the population. For R&R and A&A services, the demand scales with the number of buildings, which is correlated with the population and number of businesses. From this aspect, we can expect these services to remain in demand. Barrier to entry isn't high, but due to the labour-intensive nature of these services, new entrants will likely be smaller scale sub-contractors instead.

Nature of Expenses

As they spent $13M on their new corporate office in FY2017, the loans and depreciation expenses have just kicked in in FY18. Personally, I think that centralisation is good, considering that they had acquired many companies in the past few years and they likely had not consolidated their systems and manpower. Whether or not they can integrate everything together fast enough to control their expenses, I do not know, but the expenses do look prudent.

Net profit margin dropped to 0.9% in FY2018. I like it that this number was calculated and presented in the slides. Some companies that want to down play the decrease in net profit margin leave it to you to calculate it from the financial statements and just show you the gross profit margin. It will be good if they had stated how many years they used to depreciate their new leasehold property. It is also unknown if there are any old office premise currently parked under property assets that they will be selling away after they shift to their new office.

Earnings

Earnings per share is 0.66 cents. Dividend is 0.18 cents. Based on the last transacted price of 24 cents, it translates to Price Earning Ratio (PER) of 36 and Yield or 0.75%. This is awfully low and further price drops should be expected. The number of projects need to increase, or expenses reduced, in order for them to reap profits again.

References:

The writer owns shares in Isoteam.

The share price for this company had recently fallen a lot, because of fewer projects, reduction in suppliers' rebates (hence increased cost of sales) and increase in marketing expenses that ate into profits.

|

| Extracted from presentation slides from 4Q2018, ending 30 Jun 2018 |

65% of revenue comes from R&R and Additions and Alterations (A&A), which are rather labour-intensive. It's one of those things like a hair cut where you need hair cuts regularly and it can't exactly be automated. For hair cuts, the demand scales proportionally to the population. For R&R and A&A services, the demand scales with the number of buildings, which is correlated with the population and number of businesses. From this aspect, we can expect these services to remain in demand. Barrier to entry isn't high, but due to the labour-intensive nature of these services, new entrants will likely be smaller scale sub-contractors instead.

Nature of Expenses

As they spent $13M on their new corporate office in FY2017, the loans and depreciation expenses have just kicked in in FY18. Personally, I think that centralisation is good, considering that they had acquired many companies in the past few years and they likely had not consolidated their systems and manpower. Whether or not they can integrate everything together fast enough to control their expenses, I do not know, but the expenses do look prudent.

Net profit margin dropped to 0.9% in FY2018. I like it that this number was calculated and presented in the slides. Some companies that want to down play the decrease in net profit margin leave it to you to calculate it from the financial statements and just show you the gross profit margin. It will be good if they had stated how many years they used to depreciate their new leasehold property. It is also unknown if there are any old office premise currently parked under property assets that they will be selling away after they shift to their new office.

|

| Extracted from financial report from 4Q2018, ending 30 Jun 2018, page 27 of 29 |

|

| Extracted from financial report from 4Q2017, ending 30 Jun 2017, page 27 of 29 |

Earnings

Earnings per share is 0.66 cents. Dividend is 0.18 cents. Based on the last transacted price of 24 cents, it translates to Price Earning Ratio (PER) of 36 and Yield or 0.75%. This is awfully low and further price drops should be expected. The number of projects need to increase, or expenses reduced, in order for them to reap profits again.

References:

The writer owns shares in Isoteam.

Sunday, October 28, 2018

Book Review: Wee Cho Yaw - 黄祖耀 - 大华之道

I like the chinese title a lot more than the english title because it really reflects the contents of the book - the way of United Overseas Bank (UOB). The english title is Wee Cho Yaw - Banker, Entrepreneur and Community Leader by Pang Cheng Lian, which doesn't do justice to the book.

This book was recommended by a colleague. I was hooked onto the contents and finished reading the book within 1 man day spread over a few days. It is about the history of Wee Cho Yaw's life and some of the key business decisions that he made which made UOB what it is today. Compared with Robert Kuok's book, this book is much thinner, nothing about the war and japanese occupation, but it does show how common it was for men to have two wives in the past, how lucky they were, how their parents shaped their values (for Kuok, it was his mother, for Wee, it was his father), and how the leader' values run through the company.

Similar to Robert Kuok, Wee was also born with a silver spoon. Wee took over the bank from his father, Datuk Wee Kheng Chiang.

One thing that was mentioned multiple times was how important it was for the company staff to be focused on long term growth and results as opposed to short term results. He thinks that banks that reward staff based on annual profits and growth figures will lead staff to take on very high risks which puts the bank in an unnecessary risk position, such as loans to high risk customers, buying highly leveraged risky products, leveraged trades, etc. He claimed to reward staff more based on long term results, and as a result have many staff work for him for a very long time. He also emphasised the importance to have good leaders, and personally selects the leaders with the key characteristics of integrity to safeguard public funds and passion for the job. It sounds noble, and I really hope UOB remains like that.

Risk management in UOB is likely very conservative, given the way he describes that it is very important to win the trust of the customers, because the customers need to trust the bank in order for the bank to survive. He cited an example how a mini bank-run caused panic among the customers and staff even had to go as far as to escort a lady who withdrew tens of thousands of cash all the way to her home. The panic was caused by a misunderstanding where queues that formed at branches to pay their utilities bills was mistaken to be customers withdrawing their money. These rumours made other customers panic and when the bank branch ran out of cash, it caused even more panic to the public. It is always such experiences that live in the back of our minds that remind us the importance of building trust.

Wee also emphasised the need on passing on the values of the earlier migrant chinese and UOB, which was the motivation for this book. The migrant chinese placed a lot of emphasis of education, many contributed and continue to contribute to school building funds. Social cohesion through clans and associations were also something mainstream in the past, but not so much now because their roles had been taken over by structured education systems managed by the government. I wonder how much of chinese migrant history we can preserve when everything is so westernised.

The final chapter was one that made me reflect the more about what it means to "enjoy my job". Wee believes that to gain success, one must enjoy one's job. "The job is not important. What is important is that you enjoy doing it. You have to be passionate about your career; this is the basis of future success." However, the definition of success varies for everyone too.

He also prefers to employ people who are prepared to disagree with him when a situation warrants it. Although he is a person of strong views, the last thing he wants are yes-man who accept his ideas mindlessly. This also made me think about how the management hierarchy seem to favour yes-man nowadays.

His secret to success was summarised as luck, having the right team, and family support.

This book was recommended by a colleague. I was hooked onto the contents and finished reading the book within 1 man day spread over a few days. It is about the history of Wee Cho Yaw's life and some of the key business decisions that he made which made UOB what it is today. Compared with Robert Kuok's book, this book is much thinner, nothing about the war and japanese occupation, but it does show how common it was for men to have two wives in the past, how lucky they were, how their parents shaped their values (for Kuok, it was his mother, for Wee, it was his father), and how the leader' values run through the company.

Similar to Robert Kuok, Wee was also born with a silver spoon. Wee took over the bank from his father, Datuk Wee Kheng Chiang.

One thing that was mentioned multiple times was how important it was for the company staff to be focused on long term growth and results as opposed to short term results. He thinks that banks that reward staff based on annual profits and growth figures will lead staff to take on very high risks which puts the bank in an unnecessary risk position, such as loans to high risk customers, buying highly leveraged risky products, leveraged trades, etc. He claimed to reward staff more based on long term results, and as a result have many staff work for him for a very long time. He also emphasised the importance to have good leaders, and personally selects the leaders with the key characteristics of integrity to safeguard public funds and passion for the job. It sounds noble, and I really hope UOB remains like that.

Risk management in UOB is likely very conservative, given the way he describes that it is very important to win the trust of the customers, because the customers need to trust the bank in order for the bank to survive. He cited an example how a mini bank-run caused panic among the customers and staff even had to go as far as to escort a lady who withdrew tens of thousands of cash all the way to her home. The panic was caused by a misunderstanding where queues that formed at branches to pay their utilities bills was mistaken to be customers withdrawing their money. These rumours made other customers panic and when the bank branch ran out of cash, it caused even more panic to the public. It is always such experiences that live in the back of our minds that remind us the importance of building trust.

Wee also emphasised the need on passing on the values of the earlier migrant chinese and UOB, which was the motivation for this book. The migrant chinese placed a lot of emphasis of education, many contributed and continue to contribute to school building funds. Social cohesion through clans and associations were also something mainstream in the past, but not so much now because their roles had been taken over by structured education systems managed by the government. I wonder how much of chinese migrant history we can preserve when everything is so westernised.

The final chapter was one that made me reflect the more about what it means to "enjoy my job". Wee believes that to gain success, one must enjoy one's job. "The job is not important. What is important is that you enjoy doing it. You have to be passionate about your career; this is the basis of future success." However, the definition of success varies for everyone too.

He also prefers to employ people who are prepared to disagree with him when a situation warrants it. Although he is a person of strong views, the last thing he wants are yes-man who accept his ideas mindlessly. This also made me think about how the management hierarchy seem to favour yes-man nowadays.

His secret to success was summarised as luck, having the right team, and family support.

Tuesday, October 16, 2018

What did I buy in Aug 18, Sep 18 and Oct 18?

Gosh, 3 months zoomed past!

Aug 18

Isoteam Bought Isoteam at $0.31 without a detailed review. Prices have fallen further since (0.215 on 15 Oct), so I probably should stop procrastinating and do a proper review.

Sep 18

QAF Bought more at $0.75. Prices have fallen further since (0.725 on 11 Oct). Somehow I don't seem to be hitting the right notes although I did a detailed review in July.

Oct 18

None so far... but I am watching Capitaland Commercial Trust, SIA Engineering, Wilmar... I will probably end up putting my money in Singapore Savings Bonds temporarily as I haven't found anything really worth buying.

[Edit: bought AIMS AMP REIT in end Oct]

Aug 18

Isoteam Bought Isoteam at $0.31 without a detailed review. Prices have fallen further since (0.215 on 15 Oct), so I probably should stop procrastinating and do a proper review.

Sep 18

QAF Bought more at $0.75. Prices have fallen further since (0.725 on 11 Oct). Somehow I don't seem to be hitting the right notes although I did a detailed review in July.

Oct 18

None so far... but I am watching Capitaland Commercial Trust, SIA Engineering, Wilmar... I will probably end up putting my money in Singapore Savings Bonds temporarily as I haven't found anything really worth buying.

[Edit: bought AIMS AMP REIT in end Oct]

Sunday, August 19, 2018

Stock Review: Singapore Airlines

I last reviewed SIA in Feb 2017. Prices have since went on a roller coaster ride and it's now $9.56, last done last friday. The lowest was $9.50 on 13 and 16 Aug 2018.

Profit Margin

Profit Margin is still lean, but an improvement from previous review,

FY17 = 892.9/15806.1=5.65%

FY16 = 360.4/14868.5=2.42%

Q12018 = 149/3844.5=3.88%

Q12017 = 346.5/3864.2=8.97%

Fuel costs have been rising and adding to costs. In 2016 and 2017, fuel costs form 25% of revenue.

FY17 = 3899.3/15806=24.7%

FY16 =3747.5/14868.5=25.2%

Q12018 = 1079.4/3844.5=28.1%

Q12017 = 925.7/3864.2=24.0%

Clearly, fuel costs ate into their margins in Q12018.

Return on Assets (= Net Income/Assets)

SIA is constantly buying aircraft. They boast a young fleet with average age under 5 years old. I chose to divide by the Property, Plant and Equipment figure as it is likely referring to the aircraft, instead of total assets, which includes other investments. For this calculation, I prefer to use the more conservative net income instead of operating profit because debt is used to finance the aircraft purchase.

FY17 = 892.9/19824.6=4.5%

FY16 = 360.4/16433.3=2.2%

Overall, it's still not an effective use of the aircraft, but I guess we can say that the new aircraft may be a draw for customers.

Dividend Sustainability

Free Cash Flow per share is even more negative now at -$1.03 in Q12018. Dividend payouts are funded by debt. Although they paid a dividend of 40 cents for 2017, a yield of 4.2%, I am not attracted to it. As a whole, SIA may have been watching their costs, but I just don't think their increasing debt is a good thing.

The writer does not own any SIA shares.

References:

Profit Margin

Profit Margin is still lean, but an improvement from previous review,

FY17 = 892.9/15806.1=5.65%

FY16 = 360.4/14868.5=2.42%

Q12018 = 149/3844.5=3.88%

Q12017 = 346.5/3864.2=8.97%

Fuel costs have been rising and adding to costs. In 2016 and 2017, fuel costs form 25% of revenue.

FY17 = 3899.3/15806=24.7%

FY16 =3747.5/14868.5=25.2%

Q12018 = 1079.4/3844.5=28.1%

Q12017 = 925.7/3864.2=24.0%

Clearly, fuel costs ate into their margins in Q12018.

Return on Assets (= Net Income/Assets)

SIA is constantly buying aircraft. They boast a young fleet with average age under 5 years old. I chose to divide by the Property, Plant and Equipment figure as it is likely referring to the aircraft, instead of total assets, which includes other investments. For this calculation, I prefer to use the more conservative net income instead of operating profit because debt is used to finance the aircraft purchase.

FY17 = 892.9/19824.6=4.5%

FY16 = 360.4/16433.3=2.2%

Overall, it's still not an effective use of the aircraft, but I guess we can say that the new aircraft may be a draw for customers.

Dividend Sustainability

Free Cash Flow per share is even more negative now at -$1.03 in Q12018. Dividend payouts are funded by debt. Although they paid a dividend of 40 cents for 2017, a yield of 4.2%, I am not attracted to it. As a whole, SIA may have been watching their costs, but I just don't think their increasing debt is a good thing.

The writer does not own any SIA shares.

References:

- Financial Report Q12018, ended 30 Jun 2018

- Financial Report Q42017, ended 31 Mar 2018

Monday, July 30, 2018

What did I buy and sell in Jul 18?

QAF Limited Bought more at $0.86. I systematically bought after prices fell another 10%. This time, I did a more detailed review on the business and the factors affecting their pork business. I still believe that it is a good business although I have heard many alternate interpretations. It is one of those moments where you wonder if your analysis is wrong because everybody is selling, or the opposite...

Singapore Press Holdings (SPH) Sold at $2.90. I recommended to buy SPH when the prices fell after the next CEO took over. I recently decided to sell because it has risen 20% from it's low of $2.41 (23 Mar 2018). One of my sell criteria is when the price rises fast without any fundamental or economic changes that caused the prices to fall. Most importantly, it's to take profit first, then decide whether to by again later. Given the share price's volatility, this stock should be a good candidate to trade in and out. There should be another wave to ride when SPH launches their Woodleigh Residences condo in late Sep 2018. I will see how the prices go...

Singapore Press Holdings (SPH) Sold at $2.90. I recommended to buy SPH when the prices fell after the next CEO took over. I recently decided to sell because it has risen 20% from it's low of $2.41 (23 Mar 2018). One of my sell criteria is when the price rises fast without any fundamental or economic changes that caused the prices to fall. Most importantly, it's to take profit first, then decide whether to by again later. Given the share price's volatility, this stock should be a good candidate to trade in and out. There should be another wave to ride when SPH launches their Woodleigh Residences condo in late Sep 2018. I will see how the prices go...

Monday, July 23, 2018

Stock Review: QAF Limited

QAF Limited is a company owned by the late indonesian tycoon Mr Liem Soie Leong aka Soedono Salim who founded the conglomerate Salim Group. His youngest son Anthony runs Indofood Agri Resources, a palm oil producer. His second son Andree runs QAF as Vice Chairman, which has 3 business areas: bakery (e.g. Gardenia), primary production (pork produce, e.g. Rivalea) and distribution and warehousing (e.g. Cowhead, Farmland). Andree's son Lin Kejian runs QAF as Joint Group Managing Director. To see a more detailed listing of the brands they distribute, check out Ben Foods.

QAF has a long history (you can read a bit more about Wong Fong Fui who turned QAF's business around before selling it to Salim Group in 1996). The company focused on Gardenia bread and expanded their business from there. Bakery is still very much a core business for them.

Their share price has fallen from a high of $1.585 in Feb 2017 to the current low of $0.86 in Jul 2018, a drop of 46%. This is mainly due to a pork oversupply issue worldwide that started in the beginning of 2017 after China reduced pork imports.

So is the stock worth buying? The most important factor to assess is whether the business, excluding the affect pork business, is able to provide stable income for the company. There are many figures inside the financial report but I will drill into the earnings by segment.

References: 1Q2018, 4Q2017

The earnings from primary production is about 30% in 2017. Although the 1Q2018 report didn't state the Earnings before income tax (EBIT), based on the proportion between EBITDA and EBIT for FY2017, we can expect the primary production contribution in 2018 to be lower than 30%. Earning per share (EPS) in 1Q2018 has reduced from 2.6 cents in 1Q2017 to 0.5 cents in 1Q2018. There was also a scrip dividend issue which diluted the shareholder base slightly (1.5%).

Assuming straight-line projection of earnings for the rest of 2018, i.e. 0.5 cents x 4 quarters = 2 cents, QAF is definitely not going to be able to pay its dividend of 5 cents/year, a track record which they have been maintaining for since 2012. There is no net profit per segment figure in the financial report, which I thought would be good if the management had included it. Anyway, we need a guess-timate, so we just use whatever is available. Based on this, and assuming bakery's profit is constant, because the EBITDA figures say so, I estimate the loss from primary production to be $11M. The only problem is there is no way to tell whether this loss is a one-off or a recurring loss.

Ok, now to the valuation, if the business could be valued by the market at $1.585 at its peak, halving the price means that the market is expecting the primary production business to not contribute any income. As we have seen that the losses are actually eating into the profitable bakery business, this suggests that QAF's share price can fall further. My current average price is $1 and I will be holding on to these stocks as it has a good economic moat -- bakery and food distribution business, even if its pork business is out of business.

The pork oversupply issue is hitting US the hardest because China has imposed a 25% tax on US pork imports. Many australian pig farms have closed. Some may have to kill the pigs because there are no buyers and it costs money to feed them. The only reprieve will be if China is agreeable to take in Australian pork imports, however, this will take a while even if they start negotiations now. I am expecting QAF's price to remain volatile in the next 6 months until the market consolidates. My strategy is to just buy on dips to average down, barring any other unforeseen events like a full-blown trade war that sends everything crashing.

|

| QAF ownership extracted from SGX Stockfacts |

Their share price has fallen from a high of $1.585 in Feb 2017 to the current low of $0.86 in Jul 2018, a drop of 46%. This is mainly due to a pork oversupply issue worldwide that started in the beginning of 2017 after China reduced pork imports.

|

| QAF's share price over the past 10 years |

|

| Extracted from financial reports FY2017 and Q12018 |

The earnings from primary production is about 30% in 2017. Although the 1Q2018 report didn't state the Earnings before income tax (EBIT), based on the proportion between EBITDA and EBIT for FY2017, we can expect the primary production contribution in 2018 to be lower than 30%. Earning per share (EPS) in 1Q2018 has reduced from 2.6 cents in 1Q2017 to 0.5 cents in 1Q2018. There was also a scrip dividend issue which diluted the shareholder base slightly (1.5%).

Assuming straight-line projection of earnings for the rest of 2018, i.e. 0.5 cents x 4 quarters = 2 cents, QAF is definitely not going to be able to pay its dividend of 5 cents/year, a track record which they have been maintaining for since 2012. There is no net profit per segment figure in the financial report, which I thought would be good if the management had included it. Anyway, we need a guess-timate, so we just use whatever is available. Based on this, and assuming bakery's profit is constant, because the EBITDA figures say so, I estimate the loss from primary production to be $11M. The only problem is there is no way to tell whether this loss is a one-off or a recurring loss.

|

| Extracted from financial reports FY2017 and Q12018 |

The pork oversupply issue is hitting US the hardest because China has imposed a 25% tax on US pork imports. Many australian pig farms have closed. Some may have to kill the pigs because there are no buyers and it costs money to feed them. The only reprieve will be if China is agreeable to take in Australian pork imports, however, this will take a while even if they start negotiations now. I am expecting QAF's price to remain volatile in the next 6 months until the market consolidates. My strategy is to just buy on dips to average down, barring any other unforeseen events like a full-blown trade war that sends everything crashing.

Thursday, July 5, 2018

Book Review: Robert Kuok a Memoir with Andrew Tanzer

Robert Kuok Hock Nien is well-know businessman who ran mainly the palm oil and sugar business Wilmar and the hotel property business Shangri-La.

This book tells the tale of his early years in Johor Bahru, studying in Singapore Raffles College, and then returning to JB when the Japanese war broke out, so he didn't complete school. He was quite lucky to not get captured and earned a job in Mitsubishi during the Japanese occupation. Many chinese hated the Japanese but he didn't (for survival).

Luck was the recurring theme throughout his life, government appointed him sole distributor licenses, profiting in sugar trades, tariff protection from government, his mother's help with picking divination lots when he couldn't decide, an acquantaince that suggested the name Shangri-La for his hotel, buying prime land at discounts, living a long life despite working long hours, always rushing onto a plane, grew up smelling second smoke, smoked a bit, ... which are all lifestyle choices that are correlated with bad health.

Overall, I didn't feel that I learnt as much as from Philip Yeo's memoir, about making investments. Robert Kuok's memoir was more like how to clinch deal strategy -- put everything down and always arrive earlier than others.

He also gave his views on capitalist and communist societies. He is anti-greed, but acknowledges that greed is necessary to motivate people to work. Knowing when to stop will then be a matter of moral values. His thoughts on money is also quite similar to Warren Buffett where he said that he does not believe in leaving his wealth to his children. He sets up foundations and help the needy with the recurring income these investments are generating. He believes that if his children are like him, they won't need his money. If his children are not like him, then he will probably spoil them with his money.

I may not believe whole-heartedly that he is this very noble businessman who creates jobs and look after staff, but I do believe that his postscript message written on the last page when he was 94 years old in 2017 is genuine:

"I would like young people to take stock of what life on earth is really about. Do not confuse material satisfaction with happiness. Money cannot do everything for you. Distinguish between the real and the fanciful. Learn to live simply and, whenever you can, share your wealth with others. You are not alone in this world. There is immense wisdom handed down from ancient sages such as Laozi, who taught that to live a contented life, one should eschew greed and live as simply as possible and in harmony with nature."

Wednesday, June 20, 2018

What did I buy in Apr 18, May 18 and Jun 18?

I didn't know 3 months had passed so quickly.

Apr 18

Design Studio Bought more at $0.32. I didn't have the time to do a detailed review, but the company locked in losses, CFO resigned, but I think that the business model was still sound, so I just bought a bit first. Prices have fallen further since, so I will just adopt wait and see approach.

May 18

QAF Bought more at $0.95. Same thing, I didn't have the time to do a detailed review, but the company announced reduced earnings, some oversupply issues still persist which look cyclical, but economic moat still looks good, so I just bought a bit first. Prices have not fallen beyond $0.95, but hovering around $1.

Jun 18

Singtel Bought more at $3.18. Same thing, I didn't have the time to do a detailed review, but the company fundamentals hadn't changed much. I think it's just the market sentiment about the threat of the 4th telco adding price pressure. I still like the business, so I just bought a bit first and will just wait and see if the price falls further. Prices have fallen further.

Hopefully more opportunities appear in the coming months.

Apr 18

Design Studio Bought more at $0.32. I didn't have the time to do a detailed review, but the company locked in losses, CFO resigned, but I think that the business model was still sound, so I just bought a bit first. Prices have fallen further since, so I will just adopt wait and see approach.

May 18

QAF Bought more at $0.95. Same thing, I didn't have the time to do a detailed review, but the company announced reduced earnings, some oversupply issues still persist which look cyclical, but economic moat still looks good, so I just bought a bit first. Prices have not fallen beyond $0.95, but hovering around $1.

Jun 18

Singtel Bought more at $3.18. Same thing, I didn't have the time to do a detailed review, but the company fundamentals hadn't changed much. I think it's just the market sentiment about the threat of the 4th telco adding price pressure. I still like the business, so I just bought a bit first and will just wait and see if the price falls further. Prices have fallen further.

Hopefully more opportunities appear in the coming months.

Monday, April 9, 2018

Book Review: Building wealth through REITS by Bobby Jayaraman

I decided to read this book because I was interested to find out how the perspectives of the REIT managers were like when it was written in 2011. It is very easy to read, not many financial technical terms, and is very suitable for a REIT investor wannabe.

The first half of the book is the theory, which you will find boring if you already know how to read the items in the financial statements and fairly standard ratios. Nonetheless I learnt about perspectives. For example, when someone tells you to focus on the Net Property Income (NPI) of the REIT, it actually refers to the NPI as an amount, but what the analyst uses is the growth % of the NPI. For me, I prefer to use my version of NPI where I exclude the valuation gains but include other losses, so that I get an even lower value.

Two REITs stood out for me -- Saizen REIT and Capitaland Mall Trust. Saizen has been delisted, and I didn't know its history until I read this book. If I had known, I may have bought it. It was actually a set of distressed residential properties being bought over by investors when a Hokkaido bank went bankrupt between 1999 to 2000. These investors cashed out of their investments in 2007 via an Saizen REIT IPO. Such opportunities happen once in a blue moon for the folks who have the cash.

The history of Capitaland Mall Trust was also interesting because it explained the high valuation gains. The properties were bought from the parent Capitaland in 2002 at relatively lower prices. Over the years, they sold off the under-performing properties too. I never really thought about it that way, and by the same yard stick, Keppel REIT should have a high valuation gain too because they were created around the same time. I will probably pay more attention to this when I review Keppel REIT again.

One recurring theme discussed in the REIT managers' interviews is to only buy the property when the price is good. This can be either in the form of buying an old building at a good location and then renovating it, or to buy multiple properties located at good population catchment areas to leverage on a single management team to save on cost. This concept can be applied to anything, even hiring people for a job, but it's probably easy to say but difficult to execute because you need to be have the skill and foresight to know how to transform less desirable properties into desirable properties.

Although the market sentiment in 2011 was one where people were quite fearful of another crash given the fresh memories of the financial crisis and continued war in Iraq, anyone who had bought at 2011 prices would have profited today too.

Overall, the book reinforces my belief that any investment is good at a yield-accretive price. Patience will pay you eventually.

The first half of the book is the theory, which you will find boring if you already know how to read the items in the financial statements and fairly standard ratios. Nonetheless I learnt about perspectives. For example, when someone tells you to focus on the Net Property Income (NPI) of the REIT, it actually refers to the NPI as an amount, but what the analyst uses is the growth % of the NPI. For me, I prefer to use my version of NPI where I exclude the valuation gains but include other losses, so that I get an even lower value.

Two REITs stood out for me -- Saizen REIT and Capitaland Mall Trust. Saizen has been delisted, and I didn't know its history until I read this book. If I had known, I may have bought it. It was actually a set of distressed residential properties being bought over by investors when a Hokkaido bank went bankrupt between 1999 to 2000. These investors cashed out of their investments in 2007 via an Saizen REIT IPO. Such opportunities happen once in a blue moon for the folks who have the cash.

The history of Capitaland Mall Trust was also interesting because it explained the high valuation gains. The properties were bought from the parent Capitaland in 2002 at relatively lower prices. Over the years, they sold off the under-performing properties too. I never really thought about it that way, and by the same yard stick, Keppel REIT should have a high valuation gain too because they were created around the same time. I will probably pay more attention to this when I review Keppel REIT again.

One recurring theme discussed in the REIT managers' interviews is to only buy the property when the price is good. This can be either in the form of buying an old building at a good location and then renovating it, or to buy multiple properties located at good population catchment areas to leverage on a single management team to save on cost. This concept can be applied to anything, even hiring people for a job, but it's probably easy to say but difficult to execute because you need to be have the skill and foresight to know how to transform less desirable properties into desirable properties.

Although the market sentiment in 2011 was one where people were quite fearful of another crash given the fresh memories of the financial crisis and continued war in Iraq, anyone who had bought at 2011 prices would have profited today too.

Overall, the book reinforces my belief that any investment is good at a yield-accretive price. Patience will pay you eventually.

Saturday, March 24, 2018

Stock Review: If I were to pick a Retail Trust

I had not done a retail REIT comparison before, so I decided to do one. Here are the REITs that I selected.

- CapitaMall Trust (CMT)

- Capitaland Retail China Trust (CRCT)

- Mapletree Commercial Trust (MCT)

- Starhill Global REIT (Starhill)

- Suntec REIT (Suntec)

- Fraser Centrepoint Trust (FCT)

- SPH REIT (SPHR)

- Net income/lettable psf - how much income after deducting expenses per square foot of lettable space, the higher the better because it means I can earn more for each square foot. I also deducted the adjustments on fair value of properties (unrealised paper gains on property value) which will unnecessarily boost the earnings because it doesn't translate to cash income.

- Overall profit margin - how much income per $1 collected, the higher the better because it means expenses are lower.

- Loan interest rate - the lower the better, because it shows how the banks and debtors are perceiving the riskiness of the business.

- Occupancy - the higher the better, because it shows that demand exceeds or matches supply. This helps to ensure that rentals can be held steady or increased.

- Dividend/Earning per share (EPS) - the lower the better because it shows that the properties are sitting on large unrealised paper gains on property value.

- Debt % - the lower the better

- Yield - the higher the better, but this needs to be compared with the other similar REITs because there is a premium to pay for steady and resilient businesses.

- Price to book - how much discount the price is to market value of the properties, the lower the better because it means I get to buy the properties cheaper, but similar to yield, there is usually a premium to pay for the steady and resilient businesses. 1 means fairly valued.

|

| Comparison chart based on respective financial reports. May have data transposition errors, although I double checked most figures. |

Overall, I like CMT the best mainly because of its high income/lettable psf, profit margin, 99.2% occupancy and dividend to EPS I was half thinking why I didn't do this review earlier so that I can buy the stock at cheaper prices when REITs were having their great singapore sale.

My next favourite is SPH REIT, which I already own and this comparison re-affirms my decision. It's 100% occupancy (year after year) is what I like the best. Low debt is just a side kick. The rest doesn't really matter.

I will keep a watch on CMT and seek to add if prices recede closer to book value of $1.92.

Tuesday, March 13, 2018

My Awesome HUAT Guesses

I received an advertising mailer selling a recommended list of REITs in Singapore. When I looked at the teaser, my riddle-solving mind became very excited so I thought... it can't be that hard to guess right?

Just for fun, my awesome HUAT guesses to the riddles:

Just for fun, my awesome HUAT guesses to the riddles:

- Ascott REIT "only REIT of its kind in Singapore... 6+%" cos Keppel DC REIT doesn't meet the 6+%.

- Capitaland Commercial Trust "owns a handful of the sheer most valuable prime commercial real estate in the country"

- Capitaland Retail China Trust "10 income-producing properties (in some of China’s very best locations)"

- Capitaland Mall Trust "landlord with some 3,000 tenants"

- Ascendas REIT "manufacturing and warehouse sites ... overseas assets... loyal clients ... 6+%" would have guessed AIMS AMP if it didn't say 6+%.

- Mapletree Commercial Trust "more than 1 million square feet of the best commercial real estate in Singapore"

- Starhill Global REIT "Malaysia, this REIT boasts a portfolio of dozens of prime properties... excellent lease structure"

- SPH REIT "suburban mall play with little debt"

Any resemblance to the actual report is merely coincidental.

Any wrong guess is also unintentional.

Sunday, February 18, 2018

Stock Review: Singtel

Few years back, when Singtel prices were low, I wrote a review for Singtel in Sep 2015. I usually don't read every company's quarterly or financial report. It's a lot to read if I have to read 20 reports every quarter because I have about 20 different stocks. I usually only read up on companies which are on my shopping list and their prices are at 52-week lows, or below the past 5-years mean.

I reference Singtel's latest 3Q2018 report, i.e. 9 months ended 31 Dec 2017.

A recap of Singtel's business is that it has 3 lines of business -- Consumer (Telco), Enterprise (NCS, IT services), Digital Life and Corporate (which I will call it the rest, including rental income, start-ups, venture capital endevours), which contributes 77%, 23%, 0% profit before tax and depreciation (i.e. EBITDA on Page 31) respectively.

In the financial report, we aren't able to get a clear breakdown of telco EBITDA by geography because the report is grouped at a high-level as 100% owned and non-100% owned. Singtel and Optus are 100% owned, so the number is reported together. For the remaining telcos, they are like investments made by Singtel and the financial report itemised them and also allow you to calculate the Return on Asset for these investments. The profit (i.e. EBITDA minus depreciation, tax) by geography is available in the 2017 Annual Report (AR2017 data is 9 months old).

Although Airtel is not giving a good return, returns from Indonesia, Philippines and Thailand are good.

Income stream remains well-diversified with 70% of income sourced outside of Singapore. What could have caused Singtel prices to fall (and continue to fall) are possibly the reduced income from Airtel because Airtel is facing regulatory demands to the tune of S$3.75B (Page 28). To me, the worst case scenario is no dividends from Airtel, let's assume S$276M/year less profits. AIS (Thailand) is also facing regulatory demands of S$1.11B. Let's say we assume the worst case scenario of no dividends from AIS, then S$337M/year less profits. In 2017, net profit was $3.853B (AR2017 Page 6). If we assume worst case scenarios of 0 income from Airtel and AIS, S$3.24B and 16,344,561,000 number of shares (2Q2018 Page 20) translates to Earnings Per Share (EPS) of 23.96 cents (AR2017 Page 110) to 19.8 cents. This should not have any impact on Singtel's ability to pay 17.5 cents of dividends.

In terms of competition from the 4th, 5th, 6th Telco in Singapore, I don't think there will be much impact as these telcos will still need to rent the lines/bandwidth from Netlink Trust or existing telcos Singtel/M1/Starhub. These new players will also keep Singtel on its toes to keep cost low and retain their customers, which a definitely a good thing. The least we want is complacent monopoly giants.

In 3Q2018 Management Analysis Report, we can read some management comments. Usually management statements such as these are made together with the financial statements. Singtel separated it as a separate document probably because they furnish a lot more information than other companies would, which I like. I like their transparency, and it shows that they are also facing competition head on.

The report explained that the decrease in profit is mainly due to reduced profits from Airtel and reduced income from Netlink Trust as a result of selling Netlink Trust when compared on a year to year basis. Reduced income from Netlink Trust is expected to be seen in every quarterly report from Jul 2017, we will see this quarter-on-quarter reduction in another 2 more quarterly reports. I am personally not concerned with this because Singtel profited from the sale of Netlink Trust and lowered their debts as a result.

Debt was reduced from S$9,354M (D/E = 23.8%) to S$8,551M (22.5%). Debt/Equity (D/E) ratio is a measure of how much debt the company has as a percentage of shareholder value and retained earnings. ~20% is a good number. Singtel probably used the Netlink Trust sale proceeds to lower their debt, which is a good thing.

Singapore mobile revenue is 19% of overall revenue (Page 8). If there are worries about the competition in Singapore, M1 and Starhub are the ones who will face stiffer competition than Singtel because Singtel is the elephant in the room with 48.9% prepaid and postpaid market share (Page 53). In terms of debt, Singtel's debt is a lot lower than M1 and Starhub's. I have more details on the debt comparison in Stock Review: M1.

As at 31 December 2017, NCS’ order book increased by 25% to S$2.9 billion from a year ago (Page 33). There is no further elaboration of this, but these increases in revenue should be recognised in the next few years, and won't be immediate as IT projects typically have 1-2 years of implementation time.

Assuming a 17.5 cents dividend, at Singtel's last closing price of $3.33, it translates to a 5.25%. This is a very good yield for Singtel, considering how big an economic moat it has, diversed income streams, and stable dividend yield track record.

Major shareholder - Temasek - I bet they won't sell their stake in Singtel. It's anyone's guess how much lower prices will go. The previous low was $3.10 in 2011 but circumstances are very different now. It was $4.40 a year ago and how different were circumstances? The price has a history to have cycles and as long as we buy at the lower ends, we will have a higher margin of safety (to go wrong and make a loss). If you have extra cash, you can buy more and sell some away when the prices go up. For me, I am happy with a 5% yield.

I reference Singtel's latest 3Q2018 report, i.e. 9 months ended 31 Dec 2017.

A recap of Singtel's business is that it has 3 lines of business -- Consumer (Telco), Enterprise (NCS, IT services), Digital Life and Corporate (which I will call it the rest, including rental income, start-ups, venture capital endevours), which contributes 77%, 23%, 0% profit before tax and depreciation (i.e. EBITDA on Page 31) respectively.

In the financial report, we aren't able to get a clear breakdown of telco EBITDA by geography because the report is grouped at a high-level as 100% owned and non-100% owned. Singtel and Optus are 100% owned, so the number is reported together. For the remaining telcos, they are like investments made by Singtel and the financial report itemised them and also allow you to calculate the Return on Asset for these investments. The profit (i.e. EBITDA minus depreciation, tax) by geography is available in the 2017 Annual Report (AR2017 data is 9 months old).

|

| Data extracted from 3Q2018 Page 31 |

|

| Screen shot from AR2017 Page 2 |

In terms of competition from the 4th, 5th, 6th Telco in Singapore, I don't think there will be much impact as these telcos will still need to rent the lines/bandwidth from Netlink Trust or existing telcos Singtel/M1/Starhub. These new players will also keep Singtel on its toes to keep cost low and retain their customers, which a definitely a good thing. The least we want is complacent monopoly giants.

In 3Q2018 Management Analysis Report, we can read some management comments. Usually management statements such as these are made together with the financial statements. Singtel separated it as a separate document probably because they furnish a lot more information than other companies would, which I like. I like their transparency, and it shows that they are also facing competition head on.

The report explained that the decrease in profit is mainly due to reduced profits from Airtel and reduced income from Netlink Trust as a result of selling Netlink Trust when compared on a year to year basis. Reduced income from Netlink Trust is expected to be seen in every quarterly report from Jul 2017, we will see this quarter-on-quarter reduction in another 2 more quarterly reports. I am personally not concerned with this because Singtel profited from the sale of Netlink Trust and lowered their debts as a result.

Debt was reduced from S$9,354M (D/E = 23.8%) to S$8,551M (22.5%). Debt/Equity (D/E) ratio is a measure of how much debt the company has as a percentage of shareholder value and retained earnings. ~20% is a good number. Singtel probably used the Netlink Trust sale proceeds to lower their debt, which is a good thing.

Singapore mobile revenue is 19% of overall revenue (Page 8). If there are worries about the competition in Singapore, M1 and Starhub are the ones who will face stiffer competition than Singtel because Singtel is the elephant in the room with 48.9% prepaid and postpaid market share (Page 53). In terms of debt, Singtel's debt is a lot lower than M1 and Starhub's. I have more details on the debt comparison in Stock Review: M1.

As at 31 December 2017, NCS’ order book increased by 25% to S$2.9 billion from a year ago (Page 33). There is no further elaboration of this, but these increases in revenue should be recognised in the next few years, and won't be immediate as IT projects typically have 1-2 years of implementation time.

Assuming a 17.5 cents dividend, at Singtel's last closing price of $3.33, it translates to a 5.25%. This is a very good yield for Singtel, considering how big an economic moat it has, diversed income streams, and stable dividend yield track record.

Major shareholder - Temasek - I bet they won't sell their stake in Singtel. It's anyone's guess how much lower prices will go. The previous low was $3.10 in 2011 but circumstances are very different now. It was $4.40 a year ago and how different were circumstances? The price has a history to have cycles and as long as we buy at the lower ends, we will have a higher margin of safety (to go wrong and make a loss). If you have extra cash, you can buy more and sell some away when the prices go up. For me, I am happy with a 5% yield.

|

| Screen shot from AR2017 Page 230 |

The writers owns Singtel shares.

Friday, February 16, 2018

What did I buy in Feb 18?

Singtel I can't stress enough how good a deal Singtel is now. $3.35 screams lelong lelong and I don't know why there is so much selling. I bought more at $3.50 and $3.35. My next entry price will probably be around $3.20 if prices continues to fall. Anything below $3.50 (i.e. 5% yield) is a really good deal. 17.5 cents/year of dividends is definitely sustainable. I will say $3.80 would have been a fair price as its historical yield is closer to 4% than 5%. $3.60 would have provided sufficient margin of safety.

Wilmar I bought 1 lot only at $3.00 after much deliberation. It's a fair price, but I don't feel that I have sufficient margin of safety. I will see how it goes.

I am not sure if I will buy more in Feb, but I will monitor the situation as I had spent quite a bit these 2 months. I am also feeling slightly cash poor because I channelled $40k into Singapore Savings Bonds last month, and we aren't exactly in a market crash situation, so I won't be dipping too much into the warchest.

Wilmar I bought 1 lot only at $3.00 after much deliberation. It's a fair price, but I don't feel that I have sufficient margin of safety. I will see how it goes.

I am not sure if I will buy more in Feb, but I will monitor the situation as I had spent quite a bit these 2 months. I am also feeling slightly cash poor because I channelled $40k into Singapore Savings Bonds last month, and we aren't exactly in a market crash situation, so I won't be dipping too much into the warchest.

Tuesday, January 23, 2018

What did I buy/sell in Jan 18?

Singtel I bought 1 lot at $3.60. Fair price, not dirt cheap. Will accumulate if price dips further.

Keppel Corp I sold 1 lot at $8.16, after it gapped up consecutively and +16% over 5 days. After I sold, it continue to climb, i.e. +24% from the low of $7 after the bribery settlement news. I may cash out 1 more lot if the prices continue to gap up, to lower the concentration of Keppel Corp in my portfolio. It has been lowered from 30% to 25%.

Hyflux 6% CPS On the same day I sold Keppel Corp, I bought Hyflux 6% CPS 100 units at $91.70. I thought it was a no-brainer to buy it because the CPS redemption date is 25 Apr 2018, and the shares are going below $92. There is also a 3% dividend payment on 25 Apr. That's a total of 8% + 3% = 11% in 3 months. If Hyflux doesn't redeem the CPS, the dividend rate will be increased to 8%, which is even better right? If Hyflux doesn't redeem the CPS, they are also not allowed to pay dividends to the shareholders of the Hyflux shares. However, I dared not show-hand on this. Keep wondering if I am missing out on anything...

Stock markets around the world are hitting new highs everyday. It's feels like Apr 2015, which is the typical post financial year end reporting euphoria-effect, just that financial year end reporting has not started. This means that it can only go higher, which is probably fuelling the confidence. You would be sitting on 50% gains if you have bought the STI ETF in Feb 2016 at $2.50. Or better, you will be sitting on 80% gains if you have bought Keppel Corp in Jan 2016 at $4.70. Or even better, you will be sitting on 105% gains if you bought DBS in Feb 2016 at $13.01 (To date, I still remember this day because I was queueing at $13.00 and it didn't hit.)

Ok, enough dreaming and back to reality. It's back to the waiting game again -- waiting for the right price.

Keppel Corp I sold 1 lot at $8.16, after it gapped up consecutively and +16% over 5 days. After I sold, it continue to climb, i.e. +24% from the low of $7 after the bribery settlement news. I may cash out 1 more lot if the prices continue to gap up, to lower the concentration of Keppel Corp in my portfolio. It has been lowered from 30% to 25%.

Hyflux 6% CPS On the same day I sold Keppel Corp, I bought Hyflux 6% CPS 100 units at $91.70. I thought it was a no-brainer to buy it because the CPS redemption date is 25 Apr 2018, and the shares are going below $92. There is also a 3% dividend payment on 25 Apr. That's a total of 8% + 3% = 11% in 3 months. If Hyflux doesn't redeem the CPS, the dividend rate will be increased to 8%, which is even better right? If Hyflux doesn't redeem the CPS, they are also not allowed to pay dividends to the shareholders of the Hyflux shares. However, I dared not show-hand on this. Keep wondering if I am missing out on anything...

Stock markets around the world are hitting new highs everyday. It's feels like Apr 2015, which is the typical post financial year end reporting euphoria-effect, just that financial year end reporting has not started. This means that it can only go higher, which is probably fuelling the confidence. You would be sitting on 50% gains if you have bought the STI ETF in Feb 2016 at $2.50. Or better, you will be sitting on 80% gains if you have bought Keppel Corp in Jan 2016 at $4.70. Or even better, you will be sitting on 105% gains if you bought DBS in Feb 2016 at $13.01 (To date, I still remember this day because I was queueing at $13.00 and it didn't hit.)

Ok, enough dreaming and back to reality. It's back to the waiting game again -- waiting for the right price.

|

| Proxy indicator - STI ETF stock code ES3 |

|

| Keppel Corporation |

|

| DBS |

Subscribe to:

Posts (Atom)